news

The COVID-19 pandemic has accelerated changes to various industrial structures. In this critical period where a plunge in demand seems natural, the semiconductor industry has been placed in a state of emergency because it cannot fulfill the demand. The shortage in semiconductor supply is particularly serious in the automotive field; the consequences of the worsening scarcity in automotive semiconductors is rapidly spreading throughout the automotive industry. Semiconductors account for only about 1% of the components of an automobile; however, the current generation of cars cannot operate without semiconductors, which serve as the brain for the automotive components and engine.

The automotive industry had struggled desperately until the third quarter last year owing to the prolonged pandemic because the demand for cars decreased as businesses remained shut, restrictions were implemented on venturing outside, and social distancing was intensified to prevent the spread of viral infection. Instead, the demand for home appliances, smartphones, and IT platforms have increased as the non-contact trend was combined with repressed consumer psychology. Semiconductor suppliers have thus moved their focus of production from automotive components to home appliances and IT platforms. In the second half of last year, the demand for vehicles, which had plunged significantly, rebounded sharply in a V shape, and the semiconductor companies could not meet the suddenly soaring demand. Moreover, the low operating ratios of the raw material suppliers in the cold wave last winter played a large role in this deficit. Consequently, major automotive companies adjusted their factory operation hours or implemented production cuts. As the global scarcity of automotive semiconductors continues, the rise in semiconductor prices owing to the increase in production costs has become inevitable.

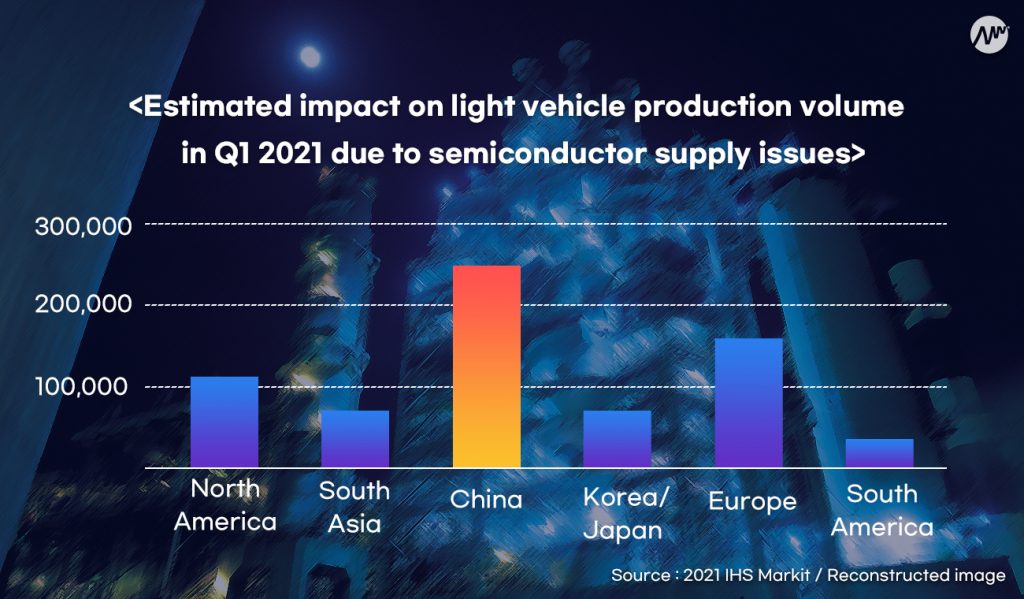

The shortage of automotive semiconductors was noticeable with the new year. The market research firm IHS Markit predicted that the automotive production shortfalls would be approximately one million units in the first quarter of this year; they originally estimated that the production shortfall would be approximately 672,000 units, but the forecast was revised significantly after 15 days. The total loss from this shortage amounts to approximately KRW 35.9 trillion considering the average car sales prices in South Korea last year. The report noted that China would suffer the largest impact, with reduced production of over 200,000 vehicles. The production losses in North America and Europe were anticipated to be over 100,000 units each.

Given these circumstances, the US, German, and Japanese governments are directly demanding the Taiwanese government to increase the production of automotive semiconductors. The semiconductor supply shock that started at the beginning of this year has now spread to the smartphone industry. The smartphone market size this year is predicted to grow by 9% from last year to 1360 million units. Amidst the pandemic, the mobile AP suppliers have reduced their production goals, thus predicting a decline in production. The smartphone market is also facing a serious semiconductor supply and demand imbalance owing to demand forecasting failure, digital transformation caused by COVID-19, and the aggressive campaigns of the Chinese smartphone makers. Drawbacks in even a single semiconductor chip could delay or prevent delivery of the substrate modules, and module production could be completely stopped in the worst-case scenario. Qualcomm, the leading manufacturer of mobile APs and communication modem chips, is also failing to meet its planned production demand owing to lack of chips, thereby negatively impacting the smartphone manufacturers.

Among them, the Chinese smartphone manufacturers who are highly dependent on Qualcomm chips were the first to be affected. This problem is increasingly becoming a test for semiconductor independence for China, which is already suffering from trade conflicts and gaps in professional semiconductor manpower. This may be the reason why the Chinese government announced plans in March to foster “third-generation semiconductors” by setting qualitative targets instead of mid- to long-term growth targets at Lianghui (Two Sessions), China’s largest political event. The reference to “third-generation semiconductor” implies a chipset using gallium nitride (GaN), silicon carbide (SiC), and gallium oxide (Ga2O3). To overcome the limitations of their semiconductor technology in the current generation, they revised the old strategy of catching up through large-scale investments into the strategy of preparing for the next-generation technology. GaN, which is considered as a representative semiconductor material of the third generation, has the properties necessary for future improvements, such as high switching speed, high efficiency, high-temperature stability, and high frequency band. Therefore, it is applied to a wide variety of applications, including 5G mobile communications, electric vehicles (EVs), data servers, wireless fast charging, and satellite communication modules.

China is strong in many technological fields, such as aerospace and AI, but has depended on imports for almost all semiconductor products ranging from non-memory semiconductors, such as APs and CPUs, to memory-based semiconductors, such as DRAMs and NAND. However, the Chinese government has recently been unable to rely on the US and has started fostering its semiconductor industry for semiconductor independence.

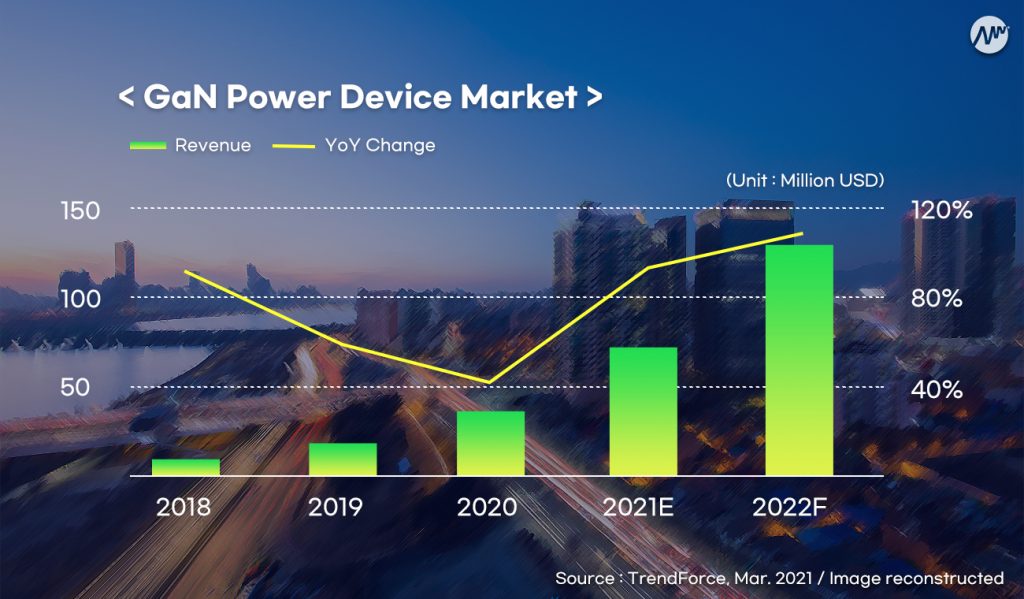

The market research firm TrendForce predicted that GaN-based power semiconductor sales would achieve a record USD 61 million (approximately KRW 68,870 million) this year, a whopping 90.6% increase from the previous year. They analyzed that the GaN-based fast charging technology, which has recently attracted attention in the smartphone market, would expand to the notebook market. The SiC power semiconductors are also known to be stable and versatile, and their market is expected to reach USD 680 million (approximately KRW 769,490 million), which is a growth of 32% from last year. TrendForce noted that telecommunications, EVs, and China would be the main growth factors for the third-generation semiconductors. They analyzed that if the Chinese production capacity for semiconductor independence were to be expanded by investing a large capital in the 14th four-year economic development plan, then the related sales would peak in 2022. Chinese companies are already investing in the semiconductor market even in the midst of a global semiconductor shortage. The automotive intelligence technology startup ECARX, which received BAIDU’s investment, announced that they have developed and would soon start mass production of 7nm chips; the largest TV manufacturer in China, TCL, also established a new subsidiary to focus on semiconductor design and new material development. TrendForce also added that the demand for 5G base stations would grow once the spread of the virus is suppressed by dissemination of the COVID-19 vaccines.

In the post-COVID era, the third-generation semiconductors are expected to jump on the bandwagon from this year. There is no clear leader in the next-generation semiconductor market yet because they are more difficult to manufacture than silicon wafers. The entire world appears to be keenly running toward this promising future semiconductor market. With this device paradigm shift, the material industry is also being observed. In South Korea, IVWorks is the only market player that is responding to the trend of new materials for third-generation semiconductors, starting the production of GaN epiwafers in 2011. IVWorks is actively connecting with high-growth applications by replacing silicon wafers, which is the existing material for DC and RF devices, with GaN epiwafers. The clients of IVWorks products include semiconductor foundries, IDMs, and domestic and international defense organizations. The company is expecting commercial sales in earnest from this year. Since this is a material development field that requires sophisticated technology and several years’ worth of knowledge and experience, the company has taken a long time to overcome the technical barriers and commercialize the materials. However, with the recent surge in market demand, leading companies in this technology are attempting commercialization more actively. IVWorks has achieved both productivity and quality by self-developing the Hybrid-MBE technology, which has large-diameter scalability and high productivity, high-quality patented semiconductor defect reduction technology, and an artificial intelligence system for production management.

At the end of last year, the DAMO Academy of Alibaba, a Chinese e-commerce company, predicted that the explosive application of third-generation semiconductors would be one of the most notable technological trends this year. Although the excellence of third-generation semiconductors has been proven, their scope of application has been limited owing to the complex processing methods and cost burden. However, their “cost-effectiveness” has increased through innovation in materials and manufacturing technologies over the past few years.

The next-generation semiconductor market, which is gradually becoming active, has emerged as a full-scale battlefield while preparing for the post-COVID era. Domestic and international semiconductor companies should focus more on the risk management of supply chains. However, the contraction of the old economy driven by the Black Swan has become a catalyst for accelerating the new economy. If we consider the current crisis as an opportunity to widen the technology gap, we may observe that the third-generation semiconductors have progressed one step farther in terms of quantity and quality in the post-COVID era.

Yoon-Seo Cho l Marketing Assistant at IVWorks

※ 본 칼럼은 기고자의 주관적인 견해로, 아이브이웍스의 공식 입장과 다를 수 있습니다.

참고문헌

- kotra, “글로벌 차량용 반도체 부족 사태, 현황과 전망”, 2021.2.19.

- 서울경제, “中 미래 경쟁력에 재정 집중투입…’3세대 반도체’ 수백조 투자, 2020.9.7.

- IHS Markit, “Managing the 2021 automotive chip famine”, 2021.2.2.

- 매일경제, “TSMC만 신났다…모바일 반도체 품귀, 삼성전자 퀄컴 비상”, 2021.3.13.

- 연합뉴스, “중국 기업들 잇따라 ‘공급 부족’ 반도체 시장 진출”, 2021.3.31.

- alibaba damo academy, “Technology Trends in 2021”